By

Gigabit Systems

October 23, 2025

•

20 min read

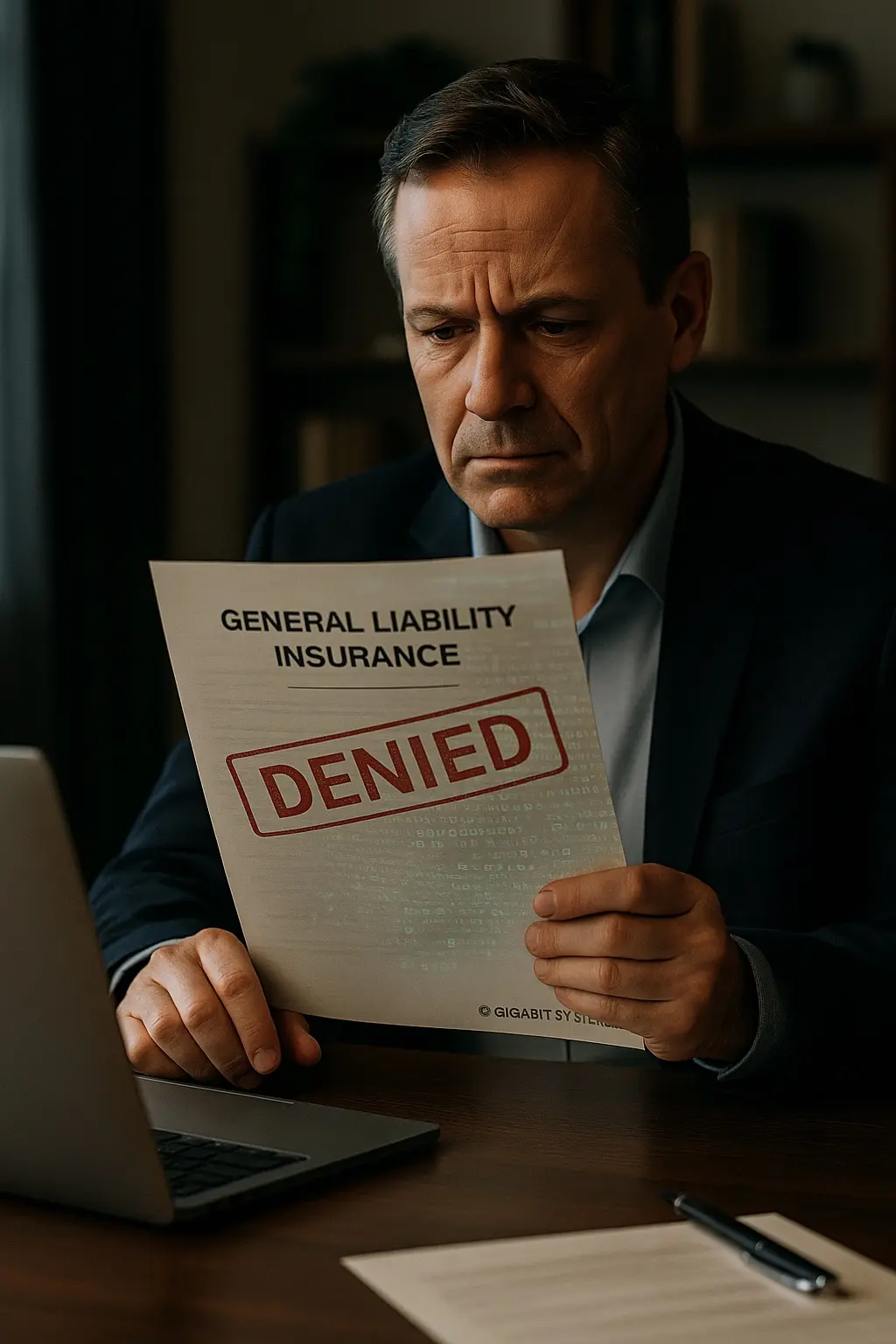

The Checkbox That Can Cost You Millions

Most businesses assume their general liability insurance will protect them from the unexpected — fires, theft, injuries, even cyber incidents.

But if your policy includes a cybersecurity rider, that protection comes with strings attached.

Insurance carriers are no longer taking your word for it. If your company claims to follow certain cybersecurity practices on paper — but doesn’t follow them in reality — you could lose coverage when you need it most.

⚠️ The Hidden Risk in That Checkbox

Every year, when renewing your general liability policy, you’ll see a section labeled something like:

“Cybersecurity Controls” or “Technology Risk Assessment.”

It’s filled with yes-or-no questions:

Do you use Multi-Factor Authentication (MFA)?

Do you conduct regular data backups?

Do you perform annual cybersecurity awareness training?

Do you patch and update your systems regularly?

Do you have endpoint protection or an incident response plan?

Checking “Yes” might feel harmless — or even expected. But here’s the truth:

✅ Each “Yes” is a legal statement.

🚨 Each false “Yes” is a liability exposure.

If your company experiences a breach and the insurer finds you overstated your cybersecurity measures, they can — and will — deny your claim.

🧩 A Costly Example

Let’s say your business has general liability insurance with a cyber rider that promises coverage for data breaches and ransomware.

During renewal, you check that:

MFA is implemented company-wide.

Backups are encrypted and stored offsite.

Employees receive annual cybersecurity training.

Six months later, you get hit with ransomware. The insurer investigates and finds:

MFA was used for email but not for remote access.

Backups were connected to the same network that got encrypted.

Staff training hadn’t been done in over two years.

Result? Claim denied.

Your general liability policy still covers physical risks — but that cybersecurity rider you paid for becomes worthless.

🏢 Why Insurers Are Getting Tougher

Cyber incidents now account for some of the most expensive claims in insurance history. From ransomware to business email compromise, payouts have exploded.

In response, insurers are demanding proof — not promises.

They now require:

Documentation of cybersecurity policies and controls

Logs showing active MFA enforcement

Evidence of employee training and response planning

Regular vulnerability scans or third-party audits

What used to be a checkbox exercise is now a compliance test.

🔒 How Gigabit Systems Helps You Stay Covered

At Gigabit Systems, we work with businesses across SMBs, law firms, healthcare, and schools to ensure their cyber practices match their insurance attestations — before renewal time.

We help you:

✅ Conduct a pre-insurance cybersecurity audit

✅ Align your actual practices with policy requirements

✅ Document your safeguards for proof during a claim

✅ Build resilience that satisfies both your insurer and your business goals

When your insurer asks, “Do you have these protections in place?” — you’ll be able to answer yes with confidence and evidence.

💡 The Bottom Line

A cybersecurity rider doesn’t guarantee protection — compliance does.

Checking the wrong box might not seem like a big deal now, but if your company experiences a breach, that small inaccuracy could cost you everything your insurance policy was supposed to cover.

So before you renew your policy this year, take a hard look at your cybersecurity practices — and make sure your answers match your reality.

⸻

70% of all cyber attacks target small businesses, I can help protect yours.

#CyberSecurity #Insurance #Compliance #MSP #RiskManagement